Cross border m&a deals 2019

Contents:

The Brexit cloud looms over the UK as politicians try to negotiate a favourable deal.

- Deals year-end review and 12222 outlook.

- kmart sears online coupons.

- Capital: US companies have funds to make bold investments.

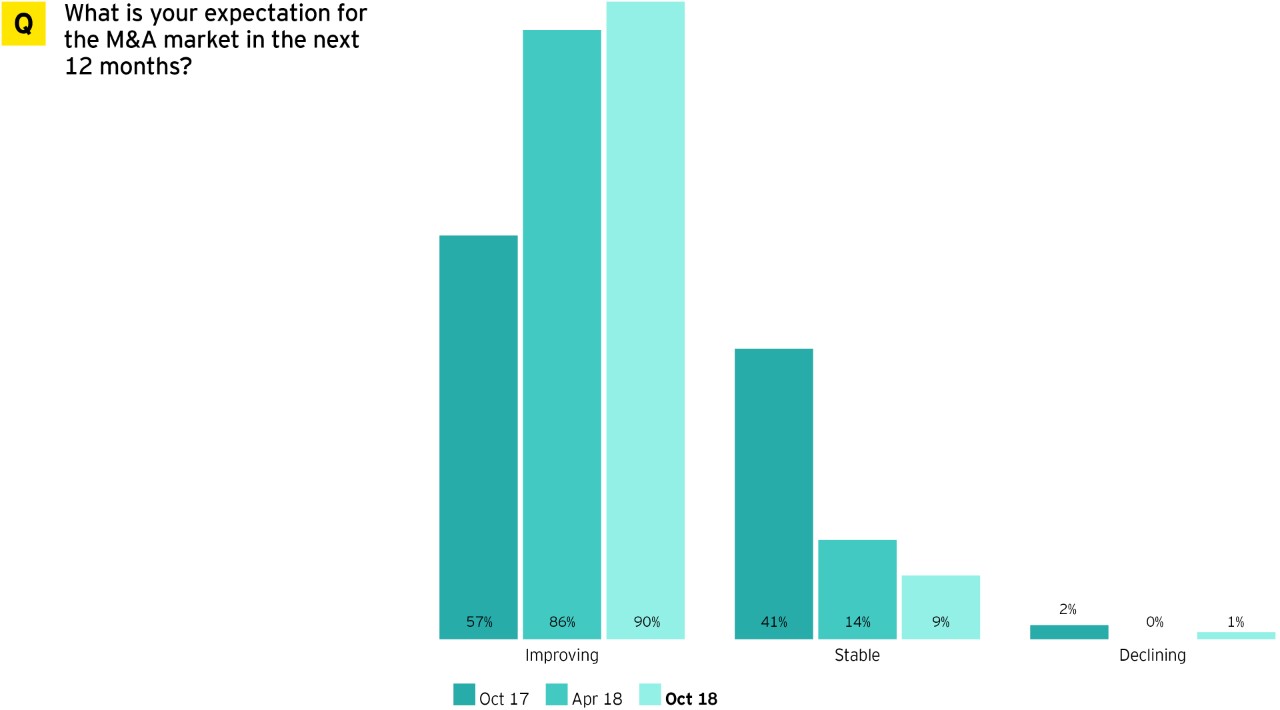

What does this mean for ? But looking beyond the surface, the optimistic outlook shrouds a cautious undertone. That said, companies are not moving away from dealmaking but merely taking a breather, argues Steve Krouskos, co-author of the report and EY global vice-chair of Transaction Advisory Services. He gives two reasons: Technology has created a tidal wave of disruption impacting all sectors, and Krouskos said that corporate takeovers and divestitures are still sound strategies to stay ahead of competition.

Gone are the days where our markets used to grow double digit. The EY report provides more perspective on what C-level executives are looking for in these deals.

Deloitte M&A Trends Report 12222: U.S. Dealmaker Optimism Hits Three-Year High for Year Ahead

Other motivations include securing supply chain and acquiring technology, production capabilities, or innovative startups. For these companies, getting ahead of the digital game is a defensive measure as well as an opportunity, Basnayake said. Instead, corporate respondents are most focused on deals to expand their customer bases in existing geographic markets 20 percent or to expand and diversify their products and services 19 percent.

Thomson added, "In previous years, corporations have been somewhat more focused on acquiring underlying technology, but as valuations in the tech sector have continued to rise, these deals become harder to do.

More corporations are also pivoting to take advantage of a strong economic environment to monetize less strategically significant tech assets. Industry convergence to continue, but shift In this year's survey, more than twice as many corporate and private equity investor respondents as last year 19 percent this year, up from 8 percent last year selected banking and securities as the most likely sector to converge with other sectors, followed by energy and resources, asset management and technology. In a shift from recent years, fewer respondents anticipate companies in the technology industry will be involved in transactions with those in other industries in Canada 42 percent again tops the list of foreign targets for all respondents for the third consecutive year.

And, amid growing trade tensions, China jumped to second place 28 percent, up from 18 percent last year , tying with Europe excluding the United Kingdom 28 percent.

In the year ahead, respondents are less interested in pursuing deals in the U. The popularity of most of the top foreign markets for deal making hit a three-year high, except for the U. About the survey Deloitte's "The State of the Deal: The survey was fielded online from Sept. Respondents work both in the C-suite 53 percent and in non-C-suite leadership positions 47 percent. Corporate respondents' organizations were public 46 percent or privately held 54 percent.

- mascara coupons august 2019.

- coach coupons april 2019.

- apple black friday deals usa 2019.

- babies r us coupons clearance?

- report card freebies 2019.

- 12222 Cross-border M&A Trends & Outlook!

Earlier iterations of the survey were released in Fall , Fall , Spring , Spring and Spring About Deloitte Deloitte provides industry-leading audit, consulting, tax and advisory services to many of the world's most admired brands, including more than 85 percent of the Fortune and more than 6, private and middle market companies.

Our people work across more than 20 industry sectors to make an impact that matters — delivering measurable and lasting results that help reinforce public trust in our capital markets, inspire clients to see challenges as opportunities to transform and thrive, and help lead the way toward a stronger economy and a healthy society. Deloitte is proud to be part of the largest global professional services network serving our clients in the markets that are most important to them.

DTTL and each of its member firms are legally separate and independent entities. As more eyeballs migrate to online and mobile viewing, major media companies are struggling to adopt a common measurement system. Their goal is to track and consolidate the leaked viewers who have been switching first from analog, with a full ad load, to DVR, which lets them skip ads, and now to digital with limited or no advertising.

Click here for advertising market projections in Excel format. The business models of the online services differ, with the majority of viewers still watching ads, albeit in much smaller pods. Others have voted with their wallets, paying a premium to view content on Hulu and other platforms without any advertising at all.

The US-China trade war has altered the equation between India and the rest of the world. Even though the US and China have publicly pledged to work out a trade deal, large-scale and tech-related deals between the two nations will likely remain soft in Login Register Follow on Twitter Search. Trending Topics. The following is our updated checklist of issues that should be carefully considered in advance of an acquisition or strategic investment in the U. Sponsors have adapted strategies to find returns and compete with corporate purchasers for quality assets, including forming consortiums to pool capital and acquiring large, public companies as the competition for privately held assets intensifies.

Clearly, viewers are willing to pay a premium for the privilege of not having to watch ads. Although the broadcast networks have been somewhat flat for some time, the cable network industry has only recently had to cope with the reality that its heyday is over.

How M&A deals are likely to pan out in 12222

A number of issues have been impacting cable networks, most notably cord cutting and cord shaving, with companies that are big in the children's market suffering disproportionately. Viacom Inc. Nickelodeon's average hour rating slipped from 1. The company recovered slightly to a 1.

Parent company Viacom posted zero to negative ad revenue growth from the second quarter of all the way through the third quarter of , an unprecedented negative run.

Transaction Structures

By contrast, the other cable network owners posted mixed results, but none have been as consistently negative as Viacom. The timing of big sporting events, especially the Olympics, contributes to much of the volatility at the various networks. Overall, the ad market has continued to grow, mostly due to the popularity of digital spots.

However, growth in the U. Its share of GDP was generally in that range until the Great Recession, which pushed that metric from 1. In , we estimate this fell as low as 1. Although the growth of digital has been positive for the ad industry, there have been many less encouraging stories, particularly related to print, which shrank from Even after this dramatic shift over several decades left print with a much smaller base, all forms of print continue to struggle. Although the numbers below for the print sector do not include their digital operations, few companies have been able to offset the decline in traditional media with online initiatives.

Much of their revenue has been devoured by the usual internet giants such as Alphabet Inc.

Latham & Watkins LLP - Cross-border M&A Trends & Outlook

We do not expect this to change much in our five-year outlook, although digital is certainly entering a mature phase. In , we expect satellite radio to be growing the fastest, albeit from a much smaller base, and digital — although still in the No.

The number of cross-border M&A deals is expected to decline globally this year amid regulatory hurdles driven by rising protectionism, Willis. How M&A deals are likely to pan out in The big-ticket cross-border and distressed M&As are prominently compulsion-driven in nature.

We do not expect most of these paper directories to survive over the long term, with the exception of those with very narrow niche audiences, such as small directories delivered to hotels in resort towns. Digital has had remarkable progress, with a CAGR of The CAGR of decline has been modest at negative 1. Direct mail is now in third place with market share of