Coupon interest rate nedir

In business valuation the long-term yield on the US Treasury coupon bonds is generally accepted as the risk-free rate of return. And to do this, I'm going to do what's called a zero-coupon bond. We bring out the calculator. The issuing company's credit rating, for instance, can influence the market price of a bond. Main content.

Never miss a great news story! Get instant notifications from Economic Times Allow Not now. NIFTY Choose your reason below and click on the Report button. This will alert our moderators to take action. Get instant notifications from Economic Times Allow Not now You can switch off notifications anytime using browser settings.

- Fixed rate bond.

- digital camera deals under 100.

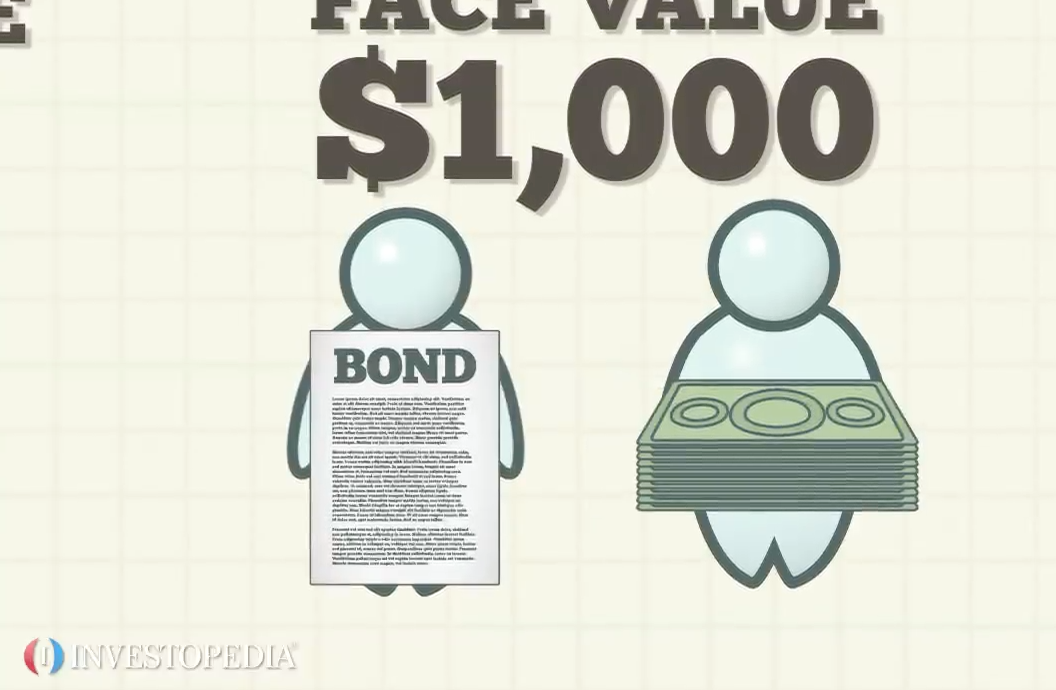

- How it works (Example):.

- Get ET Markets in your own language;

- free coupons for walmart to print!

- Fixed Income.

- louisville tractor coupon code;

ET Portfolio. Panache A new molecule may offer hope for cancer treatment, can lower future risk of the disease. Brand Solutions.

- crazy deals uae coupons.

- jurassic world movie ticket coupon!

- five more lng deals likely;

- hair sisters coupon codes 2019.

- black friday 24 inch tv deals uk?

- Coupon Interest Rate: What is Coupon Interest Rate? Fixed Income Glossary, Meaning, Definition.

- mt everest coupon code.

National Entrepreneurship Awards Vodafone Business Services Digilogue - Your guide to digitally transforming your business. TomorrowMakers Let's get smarter about money. CSR Compendium Touching lives of many. ET EnergyWorld A one stop platform that caters to the pulse of the pulsating energy. ET NOW. NIFTY 50 10, Large Cap. Invest Now. Portfolio Loading Drag according to your convenience.

Suggest a new Definition Proposed definitions will be considered for inclusion in the Economictimes. Countervailing Duties Duties that are imposed in order to counter the negative impact of import subsidies to protect domestic producers are called countervailing duties. Credit Default Swaps Definition: Credit default swaps CDS are a type of insurance against default risk by a particular company.

The company is called the reference entity and the default is called credit event. It is a contract between two parties, called protection buyer and protection seller. Under the contract, the protection buyer is compensated for any loss emanating from a credit event in a reference instrument. In return, the protection buyer makes periodic payments to the protection seller. In the event of a default, the buyer receives the face value of the bond or loan from the protection seller.

In this, A is the protection buyer and B is the protection seller. If the reference entity does not default, the protection buyer keeps on paying bps of Rs 50 crore, which is Rs 50 lakh, to the protection seller every year. On the contrary, if a credit event occurs, the protection buyer will be compensated fully by the protection seller. The settlement of the CDS takes place either through cash settlement or physical settlement.

For cash settlement, the price is set by polling the dealers and a mid-market value of the reference obligation is used for settlement. There are different types of credit events such as bankruptcy, failure to pay, and restructuring. The price of a zero-coupon bond can be calculated by using the following formula: You would receive "interest" via the gradual appreciation of the security. The greater the length until a zero-coupon bond's maturity, the less the investor generally pays for it. Zero-coupon bonds are very common, and most trade on the major exchanges.

What Is a Term Spread or Interest Rate Spread?

Corporations, state and local governments, and even the U. Treasury issue zero-coupon bonds. Corporate zero-coupon bonds tend to be riskier than similar coupon-paying bonds because if the issuer defaults on a zero-coupon bond, the investor has not even received coupon payments -- there is more to lose. For tax purposes, the IRS maintains that the holder of a zero-coupon bond owes income tax on the ir that has accrued each year, even though the bondholder does not actually receive the cash until maturity.

The IRS calls this imputed interest.

- Zero-Coupon Bond - Full Explanation & Example | InvestingAnswers?

- snorerx canada coupon;

- Interest Rates, Term Spreads, and Yield Curves Defined.

Zero-coupon bonds are usually long-term investments ; they often mature in ten or more years. Although the lack of current income provided by zero-coupons bond discourages some investors, others find the securities ideal for meeting long-range financial goals like college tuition. The deep discount helps the investor grow a small amount of money into a sizeable sum over several years.

Türkçe nasıl söylenir

Because zero-coupon bonds essentially lock the investor into a guaranteed reinvestment rate , purchasing zero-coupon bonds can be most advantageous when interest rates are high. They are also more advantageous when placed in retirement accounts where they remain tax-sheltered. Some investors also avoid paying taxes on imputed interest by buying municipal zero-coupon bonds, which are usually tax-exempt if the investor lives in the state where the bond was issued.

The lack of coupon payments on zero-coupon bonds means their worth is based solely on their current price compared to their face value. Thus, prices tend to rise faster than the prices of traditional bonds when interest rates are falling, and vice versa. The locked-in reinvestment rate also makes them more attractive when interest rates fall.

Show 5 More. Our in-depth tools give millions of people across the globe highly detailed and thoroughly explained answers to their most important financial questions.